Retirement is an important milestone

We want you to enjoy your retirement years to the fullest. That’s why we offer a pension plan that works together with government benefits and your personal savings to provide the income you’ll need to make the most of this special time of your life.

Snapshot

How does the plan work?

Your pension plan works a lot like a Registered Retirement Savings Plan (RRSP). You and the University contribute equal amounts to a pension account set up in your name. The money is invested and grows tax-free until you retire and use it to pay yourself a retirement income.

Who can join?

You are required to join the plan if you are an In-Scope or Out of Scope Faculty/Senior Administrative employee (employed half time or more) and you have:

- a probationary appointment leading to permanent status, or

- a term appointment of greater than 6 months, or

- a without-term appointment for an expected duration greater than 6 months, or

- been granted tenure

You are required to join the plan if you are an In-Scope Administrative or Exempt employee (employed half time or more) and you have a:

- permanent appointment, or

- term appointment greater than 6 months

How do I contribute?

Contributions are made automatically through payroll deductions.

How are contributions invested?

You make the investment decisions for all contributions to your account, choosing from eight different investment funds.

When can I retire?

Early retirement starts June 30th on or following your 55th birthday. Normal retirement starts June 30th on or following your 67th birthday.

You can also postpone your retirement. However, you must transfer your account balance out of the plan before December 31st of the year you turn age 71.

Are there admin fees?

Plan members are charged administration fees, which are automatically deducted from your account. The fees are:

- $130 annual ($10.83/month) Sun Life administrative fee

- Two basis-point (0.02 per cent) annual USask administrative fee

- Three basis-point (0.03 per cent) annual Sun Life Target Date Fund administrative fee*

- Two basis-point (0.02 per cent) annual Aon Target Date Fund administrative fee*

In addition to the administration fees, investment management fees are also automatically charged. Investment management fees vary by investment option – for a detailed list of investment management fees, please visit mysunlife.ca.

* Charged only on balances invested in Target Date Funds.

The pension plan is one of the best deals around when it comes to tax savings. Your contributions are tax deductible and you don’t pay tax on the investment income you earn. You’re only taxed when you retire and begin to withdraw money from your pension savings.

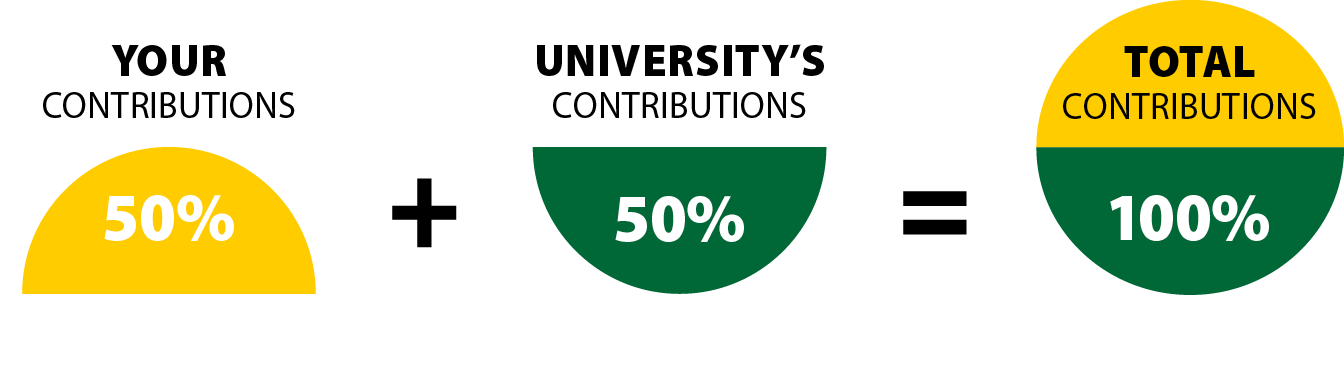

Contributions

The pension plan makes it simple to save for retirement. Your contributions are automatically deducted from each pay and you also get the benefit of an equal contribution from the University.

How much will you and the University put in? It all depends on your position.

| Position | Your contribution | University’s contribution | Total contribution amount per year |

|---|---|---|---|

|

Academic employees |

8.5%

|

8.5%

|

17.0%

|

|

Senior Administrative employees |

8.5%

|

8.5%

|

17.0%

|

|

Administrative and Supervisory Personnel Association (ASPA) |

7.0%

|

7.0%

|

14.0%

|

|

Exempt employees |

7.0%

|

7.0%

|

14.0%

|

Contributions are a percentage of your pensionable earnings. Pensionable earnings include your regular salary, excluding earnings such as honorariums, fees and summer session payments. Pensionable earnings are subject to a yearly maximum.

The total of your contributions and the University’s contributions cannot exceed the limit set by CRA each year. For more details, please visit www.canada.ca.

Investing

Take Control

Once contributions are deposited into your pension account, you take control! You get to decide how to invest the contributions based on your own needs and preferences. You can track and manage your investments, online, at any time at mysunlife.ca.

There are six investment funds available to you. Each one comes with a different degree of risk and return and may be right for different points in your career.

To keep things simple, the six investment funds are categorized into two main types:

Help Me Do It

We point you toward an easy investment and you make one decision.

This approach makes investing simple. It’s perfect if you don’t want to spend a lot of time managing your funds or don’t have a lot of investment knowledge.

- USask uses Target Date Funds to simplify investing for anyone with long-term savings objectives, such as retirement.

- Target Date Funds take into account your proximity to retirement and automatically adjust your portfolio to take on less risk the closer you get to age 65 (a typical retirement date).

Let Me Do It

You handle the investing and decisions using our tools.

This approach lets you build your own mix of funds based on your financial goals, your comfort with risk, and your life stage.

- Choose a combination of funds that you’re comfortable with. The Asset allocation tool can help.

- Decide how much to invest in each fund. You should review this regularly. You may need to change the amount you have in each fund from time to time.

- Actively manage your investments.

- Sign in to mysunlife.ca, select Manage plan > my plan > Make a change > Change investments

If you don’t choose an investment option(s), all contributions will automatically be invested in the Target Date Fund closest to the year you turn 65.

Sun Life's Guaranteed Daily Interest Account (GDIA)

The Academic Money Purchase Pension Plan has added Sun Life's Guaranteed Daily Interest Account (GDIA) in addition to Sun Life's Money Market (MM) fund. Members have the option to move their money into the new GDIA through their Sun Life account.

Sun Life's Guaranteed Daily Interest Account (GDIA) credits interest on a daily basis while still providing the withdrawal flexibility of a money market fund. Besides generating higher returns, the GDIA includes up to $200,000 worth of Assuris and CDIC investor protection. In comparison, Sun Life's Money Market account is exposed to normal investment market risks.

In addition, there are no explicit fees applicable to this account. Expenses and client servicing costs are fully reflected within the interest rate credited by the account.

Investing doesn’t have to be complicated! Once you join the pension plan, you get access to mysunlife.ca, where you’ll find easy-to-use online tools and resources.

The biggest help in choosing your investment funds—especially if you’re new to investing—is Sun Life Financial’s asset allocation tool. In a matter of minutes, the tool can help you determine your risk profile and the mix of funds best suited to you.

You can manage your pension account anywhere, anytime with Sun Life’s mobile app! When you download the mysunlife.ca app on your Android or Apple device, you’ll be able to view your pension plan accounts, manage your investments, and more! The app is free—simply download it from Google Play or the Apple App Store.

Retirement Options

You’ve earned your retirement, now it’s time to enjoy it! When you retire, it’s up to you to decide what to do with your pension account balance.

Prescribed Registered Retirement Income Fund (PRRIF)

Maybe you’ll live off some other income for a couple months and ramp up your withdrawals a little later down the road. A prescribed registered retirement income fund (PRRIF) lets you withdraw the amount of money* you need on a regular basis, while keeping the bulk of your savings invested at the same time.

*You can withdraw as much as you want/need (there is no maximum); however, minimum withdrawal amounts apply.

Fast Fact

The University of Saskatchewan Group Retirement Fund is a custom PRRIF available to you. You can choose from the same great investment funds available to active plan members and benefit from the same low investment management fees.

Locked-in Retirement Account (LIRA)

No problem! You can leave it in the plan or transfer it to a locked-in retirement account (LIRA). Just keep in mind—you’ll need to move the money out of the plan or LIRA to a PRRIF or to purchase a life annuity before December 31 of the year you turn age 71.

Life Annuity

You may want to consider purchasing a life annuity from an insurance company. You will receive an annuity payment every month, for as long as you live. You can also continue a portion of your annuity to your spouse if you pass away first.

You’re entitled to your pension account balance; however, the money will be locked-in until retirement. There are lots of options for your pension savings: you can transfer your money to a LIRA or transfer to another employer’s pension plan, purchase a deferred life annuity, or leave your money in the plan to be transferred at a later date.

The big picture

For most plan members, your University pension will be just one part of your retirement income. The rest will come from government benefits, like the Canada Pension Plan (CPP) and Old Age Security (OAS), and personal savings.

Group Retirement Fund

The Group Retirement Fund is sponsored by the University of Saskatchewan in conjunction with Sun Life Financial for members of the Academic Money Purchase Pension Plan and Research Pension Plan and will offer a Prescribed Registered Retirement Income Fund (PRRIF) and several other retirement vehicles, where applicable.

The main purpose of the Group Retirement Fund is to provide members who are retiring under the Academic Money Purchase Pension Plan and Research Pension Plan, a viable, seamless and cost-efficient alternative to transferring their pension funds to a PRRIF in the market place to provide a retirement income.

How does this affect you?

All members of the Academic Money Purchase Pension Plan and the Research Pension Plan who are retiring may transfer their pension contributions to the University of Saskatchewan Group Retirement Fund. You will be able to purchase a PRRIF through the Group Retirement Fund and invest your funds in any of the eight investment options in the Group Fund.

If you have any questions about the Group Retirement Fund, please contact the Pension Office.

USask has a retirement channel in PAWS that is full of valuable information for faculty and staff who are considering retiring in the next 2-3 years, including benefit options after retirment and a checklist to follow?

Stay Involved

Planning for retirement is important no matter what age you are. This checklist can help ensure that you’re taking care of your pension plan responsibilities.

Review the enrolment package and submit your enrolment form

Once you become eligible, you’ll receive an Academic Money Purchase Pension Plan enrolment package. Read the information so you understand how the plan works and how it fits into your overall retirement plan. Then, complete and submit the enclosed enrolment form.

Note: If you have a spouse, your spouse must be named your beneficiary.

Choose your investments carefully

Sun Life Financial is the record keeper for the pension plan. You’ll use mysunlife.ca to select, track and manage your investments. Be sure to use the online tools to help you understand your personal tolerance for risk so you can select investments that suit you best. Seek advice from a professional financial advisor if you need help.

Monitor your investments and make changes as needed

Ensuring that you’re saving enough for retirement takes careful planning and sound financial management. Review your pension plan investments from time to time and make changes as needed based on your evolving risk profile. You should also review your overall retirement savings at least once a year, with the assistance of a professional financial advisor if necessary.

USask's Checklist

The University is responsible for overseeing, managing, and administering the Academic Money Purchase Pension Plan to make sure the fiduciary and other obligations of the plan are met. It also makes sure the plan operates in compliance with the Canadian Association of Pension Supervisory Authorities’ (CAPSA) guidelines,* the Pension Benefits Act and the Income Tax Act. Details are available from the Pensions Office and in the Pension Plans section of the Financial Services Division website.

*CAPSA: an interjurisdictional association of pension regulators whose mission is to facilitate an efficient and effective pension regulatory system in Canada.

Education

Other Information

Plan Information

- Retirement channel in PAWS

- Overview

- Expense Policy

- Financial Statements

- Governance Document

- Investment Policy

Annual Reports and General Meetings

Forms

- Change in Beneficiary

You can view your current beneficiaries by logging into your Sun Life account and selecting Beneficiary info.

Glossary

Beneficiary: The person you designate to receive death benefits from the Plan after you die.

Canada Revenue Agency Limits: USask pension plans are Registered Pension Plans, governed by pension legislation and subject to the rules of The Federal Income Tax Act. As a result, there are limits to the amount you can contribute. These limits are:

- 2026: $35,390

- 2025: $33,810

- 2024: $32,490

- 2023: $31,560

- 2022: $30,780

Canada Pension Plan (CPP): The Canada Pension Plan is a federal government program based on earnings-related contributions. It is indexed annually based on the change in the Consumer Price Index. Benefits start when you reach age 65 but may begin as early as age 60. CPP also includes other benefits: a death benefit, a survivors’ pension, and disability benefits before you retire.

Continuous Employment: Continuous Employment is your most recent, uninterrupted period of employment with the University as a permanent employee. Continuous Employment is not interrupted during periods of approved absence, including:

- jury duty

- authorized vacations and statutory holidays

- authorized absences (including sabbatical leave and administrative leave)

- qualified disability; or

- breaks of less than six months between termination of employment and re-employment with the University, provided you have not taken a refund of the contributions.

In all other cases, Continuous Employment is interrupted by termination of employment, retirement, or failure to return to work following an approved absence or disability.

Life Annuity: A lifetime pension purchased through a contract with an insurance company. You receive monthly payments, the amount of which will vary depending on the type of annuity you select, the interest rates in effect when you sign the contract, and your age and your Spouse’s age when the annuity payments begin. The higher the interest rates and the older you are when payments begin, the higher the pension you will receive.

Locked-in Retirement Account (LIRA): Upon termination, you can transfer your pension plan benefits to a Locked-in Retirement Account (LIRA). A LIRA is an investment account in which you can keep your money invested. You cannot make withdrawals from your LIRA. When you reach the age of 55, and any time thereafter until you turn 71, you can use your LIRA to purchase a Prescribed Registered Retirement Income Fund (PRRIF) or a Life Annuity. You must transfer your LIRA to a PRRIF, or use it to purchase a Life Annuity before December 31 of the year in which you turn 71.

Old Age Security (OAS): Old Age Security is a government benefit that any person 65 or older is entitled to receive after meeting certain minimum residency requirements.

Pension Adjustment (PA): The value Canada Revenue Agency assigns to your benefit under the Pension Plan. Your PA will reduce your RRSP contribution room.

Pensionable Earnings: Pensionable Earnings refers to your University salary. It excludes any other earnings such as honorariums, fees, and summer session payments, and is subject to a yearly maximum. For members of the clinical medical staff, Pensionable Earnings is the academic component of the University salary only.

Postponed Retirement: Retirement date after your Normal Retirement Date.

Prescribed Registered Retirement Income Fund (PRRIF): If you are 55 years of age or older, upon retirement you can transfer your pension plan benefits to a PRRIF. A PRRIF allows you to keep your money invested but there is a minimum amount that must be withdrawn each year. There is no maximum withdrawal amount. Your spouse, if you have one, must sign a release in order for you to transfer your benefits to a Prescribed RRIF.

Registered Amount: Money is viewed as registered if the amount falls within Income Tax Regulations. It can be transferred on a tax-deferred basis to a registered savings vehicle. Investment income is tax-sheltered. Any withdrawals are taxable.

Registered Retirement Savings Plan (RRSP): A tax-deferred retirement savings vehicle. Contributions are tax-deferred up to Canada Revenue Agency limits. Investment income is tax-deferred. Any withdrawals are taxable.

Spouse: A person who is either:

- married to a member, or

- if a member is not married, a person with whom the member is cohabiting in a conjugal relationship at the relevant time and who has been cohabiting in a conjugal relationship continuously with the member as his or her spouse for at least one year prior to the relevant time.

Year’s Maximum Pensionable Earnings (YMPE): The earnings base used to determine Canada Pension Plan contributions and benefits. The level adjusts annually to keep pace with average wage increases in Canada.

Contact

Pension Office

- plan documents

- retirement information

- beneficiary changes

ConnectionPoint

- help with completing your enrolment form

Sun Life Financial

- changes to investments

- online account support